The goods and services tax (GST) is a broad-based tax of 10% on most goods, services, and other items sold or consumed in Australia.

GST is an indirect tax that is paid at each step in the supply chain, however, one of the principles of the GST program is that the cost of GST is borne by the final consumer. This is achieved by refunding the business for any GST it has paid in the operations of the business.

Generally, GST-registered businesses will:

- include GST in their selling prices

- claim credits for GST included in the business purchases when lodging the BAS

GST Principles

| GST collected | - | GST input tax credits | = | net GST payable |

|---|---|---|---|---|

| What your customer paid you | - | What GST you paid to make the sale | = | The GST portion of your GST liability to the ATO |

GST collected - This is the amount of money your business has collected to cover your GST obligations on the goods and services you have sold.

For example:

Kumar sells various items, including fresh fruit and vegetables, sandwiches, and imported specialty food items. He had to learn what the GST classifications are for each category of item. He followed the ATO’s GST food guide (NAT 3338) to learn them.

He adds the cost of his GST obligation to the item's price. When he records the sale in his books, he will record the GST portion in a separate account, just for GST collections.

Kumar notes the portion of GST for each sale on the customer's docket for transparency as required by the ATO because the sale amount was $118.00.

GST input tax credits - These represent the financial credits for the GST included in the cost of the purchases you make in the operations of your business. Because one of the principles of GST is that it's paid by consumers, not businesses, you can claim back the GST you have paid for things you bought to produce and sell your items or services. You may also be entitled to claim back money for fuel used in machines and large vehicles.

For example:

For Kumar to make sandwiches and soup to sell in his store, he needs specialty ingredients, which he purchases from a local restaurant. The GST portion of his cost for those items becomes GST input tax credits. Kumar carefully stores all of his invoices, receipts, and dockets.

net GST payable - This represents the difference between the GST collected and the input tax credit, the result of which is the amount of your GST obligation owed to the ATO.

For example:

Kumar receives his BAS statement from the ATO and lodges it monthly. On it, he records the total amount he is holding in his GST collected account and claims his input tax credits. He pays the ATO the difference between the two by the due date noted on the BAS statement.

GST-related terms and definitions

Some terms used in this section may be new to you or have a specific meaning in GST law. Whenever the following words and terms are used in this section they should be interpreted as shown below.

- Australia: Indirect tax zone

- Aggregated turnover: Business turnover plus the turnover of closely associated entities

- You: You as a business, for example, a sole trader, a partnership, a trustee (of a trust or a superannuation fund), or a company

- Business: The GST term enterprise

- GST turnover: The turnover figure you use to work out if you need to be registered for GST (GST turnover does not include the turnover of businesses you are connected with)

- Sales: The GST term supplies

- Purchases: The GST term acquisitions

- Payment (made or received): The GST term consideration

- GST credit: The GST term input tax credit

- Property: The GST term real property.

| Acquisition | For GST, a purchase or acquisition includes the acquisition of goods or services such as trading stock, a lease, consumables, and importations. |

|---|---|

| Business asset | A business asset is something you use for your business, for example, manufacturing equipment, a delivery van or an office computer. Intangible items, such as goodwill, may also be business assets. You generally incur a GST liability when you sell a business asset. |

| Business (enterprise) | An enterprise includes a business. It also includes other commercial activities but does not include the following:

It includes the activities of entities such as charities, deductible gift recipients, religious and government organisations, and certain non-profit organisations. |

| Consideration | Payment for GST purposes is anything you receive for providing goods, services, or anything else. Payment is usually money but can be in the form of other goods or services, as in the case of barter transactions. Payment may also be made by way of refraining from doing something. |

| Financial acquisition | A financial acquisition is an acquisition that relates to the making of a financial supply (other than a borrowing). |

| Financial acquisitions threshold |

The purpose of the financial acquisitions threshold is to allow entities that make a relatively small amount of financial supplies, as compared to their taxable supplies or GST-free supplies, to claim full GST credits relating to those financial acquisitions. If you make financial sales without exceeding the financial acquisitions threshold – for example, you make both financial and other sales and your financial sales are only a small part of your total sales – you can claim GST credits for your purchases that relate to making those financial sales (providing you have a tax invoice). |

| Financial sales (supplies) | Financial sales (supplies) are input taxed, provided certain requirements are met. A financial sale (supply) is the provision, acquisition or disposal of an interest listed in the GST Regulations. Examples include the following:

|

| GST credits (input tax credits) |

You can claim a credit for the GST included in the price of goods or services (the inputs) you buy for use in your business unless you use the purchase to make input-taxed sales. If you use the purchase partly for private purposes, you will not be able to claim a credit for the full amount of GST, only for the amount that relates to business use. |

| GST-free sales |

Some goods and services are not subject to GST and are sold without GST in their price. These sales are referred to as GST-free sales. Examples of GST-free sales include basic food, exports, sewerage, and water; the sale of a business as a going concern; non-commercial activities of charities; and most education, health, and care services. If you sell GST-free goods or services, you are entitled to credits for the GST included in the price of your “inputs” (the goods or services you used to make the goods or services you sold). |

| GST turnover threshold | GST turnover thresholds are used to work out whether you:

|

| Inbound intangible consumer sale (supply) | “Inbound intangible consumer supply” means sales of anything other than goods or real property to an Australian consumer. It doesn’t include things done wholly in Australia (the indirect tax zone), or sales made wholly through a business (enterprise) carried on in Australia (the indirect tax zone). |

| Indirect tax zone | “Indirect tax zone” means Australia, but does not include external territories and certain offshore areas. The Goods and Services Tax (GST), the Wine Equalisation Tax (WET), and the Luxury Car Tax (LCT) operate in the indirect tax zone. The GST, WET, and LCT do not operate in Australian external territories and certain offshore areas. |

| Inputs | The goods or services you use in your business to make the goods or services you sell are referred to as your inputs. |

| Input-taxed sales |

Some goods and services are sold without GST in their price, even though GST was included in the price of the inputs used to make or supply them. These sales are referred to as input-taxed sales.

In special cases, you may be entitled to a GST credit for a purchase that relates to making financial supplies. |

| Limited registration entity | If you are a non-resident, you may choose to be a limited registration entity for GST purposes if you have made, or intend to make, one or more inbound intangible consumer sales. If you choose to be a limited registration entity, you are not entitled to GST credits for purchases, and you must have quarterly tax periods. |

| Margin scheme |

You can choose to use the margin scheme when you make a taxable sale of property. GST to be paid is one-eleventh of the margin for the sale and not the normal one-eleventh of the sale price. However, you cannot use the margin scheme in certain circumstances, for example, if you purchase the property through a taxable sale where the GST was worked out without applying the margin scheme. You cannot claim a GST credit for a purchase made under the margin scheme even though you may have paid GST on the margin. |

| Payment (consideration) | Payment for GST purposes is anything you receive for providing goods, services or anything else. Payment is usually money but can be in the form of other goods or services, as in the case of barter transactions. Payment may also be made by way of refraining from doing something. |

| Property (real property) | Property includes the following:

|

| Recipient-created tax invoices | In most cases, tax invoices are issued by the supplier. However, in special cases, you, as the purchaser or recipient of the goods or services, may issue yourself a tax invoice. This is known as a recipient-created tax invoice (RCTI). |

| Reduced-credit acquisitions | Reduced-credit acquisitions are purchases (acquisitions) of some types of things that relate to making input-taxed financial supplies. You can claim a reduced GST credit on reduced-credit acquisitions. The reduced GST credit is generally 75% of the full GST credit to which you would otherwise be entitled, although in some instances relating to recognised trust schemes, the reduced credit is 55% of the full GST credit. |

| Sale of a business as a going concern | A business is sold as a going concern if:

|

| Sales (supplies) | For GST, a sale or supply includes:

|

| Self-assessment | The self-assessment system for indirect taxes began on 1 July 2012. When you lodge an activity statement for tax periods that begin on or after that date, you will still need to include the indirect tax payable amounts and any credits that make up your net amount. The Commissioner is taken to have made an assessment based on that net amount on the day you lodge the return. Your return is treated as a notice of assessment signed by the Commissioner and issued on the day the return is lodged. |

| Taxable sales | Sales of goods and services that must have GST included in their price are referred to as “taxable sales”. You make a taxable sale if you are registered or required to be registered for GST and:

|

| Tax invoice | A tax invoice is a document generally issued by the seller. It shows the price of a sale, indicating whether it includes GST, and may show the amount of GST. You must have a tax invoice before you can claim a GST credit on your activity statement for purchases of more than $82.50 (including GST). |

| Tax period | For GST purposes a tax period may be a month, a quarter, or a year and refers to how frequently you lodge your activity statements. |

Rules around GST

- A business must register for GST if either the current or projected GST turnover is $75,000 or more.

- Whenever a business purchases goods and services, a 10% component for GST will usually be included in the purchase price.

- When the business subsequently on-sells such goods and services (generally after having added value), it also has to include in the sales price a 10% component for GST.

- To stop the obvious double taxation, any GST charged on the subsequent sale (referred to as ‘outputs’) can be remitted to the ATO after deducting any GST previously paid on purchases (referred to as ‘inputs’).

- A good way to conceptualise it is to think of GST as a consumer tax on the end-user rather than a business tax.

- A business registered for GST must lodge a business activity statement which will help to report and pay goods and service tax and to claim GST credits.

GST legislation

On 1 July 2000, a 10% Goods and Services Tax (GST) started full operation in Australia. The introduction of GST was accompanied by a series of other tax measures forming part of the “New Tax System”.

The New Tax System (Goods and Services Tax) Act 1999 (Cth), known as the GST Act, was passed on 28 June 1999. Section 7-1(1) sets out the GST guidelines, setting down the rules of what is taxable and what is free or input taxed and any special rules. ;

According to Division 9-5 of the GST Act, a taxable supply arises (i.e. GST is charged) if:

- It was made for consideration

- The supplier is registered or required to be registered

- It is made in the course of carrying on an enterprise

- It is connected with Australia

- It is not GST-free or input taxed.

According to Division 11-5 of the GST Act, a credible acquisition arises (i.e. an entity can claim back the GST paid) if:

- The entity provides or is liable to provide consideration for the supply

- The entity is registered or required to be registered

- The entity acquires anything

- The acquisition was solely or partly for a creditable purpose

- The thing supplied was a taxable supply (see above).

According to Section 23-5 of the GST Act, an entity must register for GST if:

- It carries on an enterprise and

- Its GST turnover meets the registration turnover threshold

or - As a non-profit organisation it has a GST turnover of $150 000 per year or more

or - It provides taxi or limousine travel for passengers in exchange for a fare as part of the business, regardless of GST turnover – this applies to both owner drivers and if the entity leases or rents taxis

or - It wants to claim fuel tax credits for the business or enterprise.

If a business or enterprise does not fit into one of the above categories, registering for GST is optional. Should a business elect to register, it generally must stay registered for at least 12 months.

How the GST system works

The Australian Consumer Law (ACL) under the Competition and Consumer Act 2010 (Cth) aims to protect consumers and ensure fair trading in Australia. It prohibits misleading or deceptive conduct. Therefore, all prices of goods must be inclusive of all taxes and charges.

A business will charge GST for the goods and services it sells. Then it must lodge a business activity statement which is used to report and pay goods and service tax and to claim GST credits.

A business can claim a credit for any GST included in the price of any goods and services you buy for your business. This is called a GST credit (or an input tax credit). In other words, if you purchase cotton to make clothes, you will pay GST to the cotton supplier, but you will receive credits for that purchase. ;

The table below follows the GST cycle of a high-end T-shirt. ;

| Raw materials | ; | Net GST to pay | ; | What happens | ||

|---|---|---|---|---|---|---|

| A cotton grower sells cotton for $110 including $10 GST | ; | GST on sale | $10 | Cotton grower pays $10 GST to ATO | ; | The cotton grower needs to make $100 on the sale of cotton. He sells the cotton for $110, keeps $100 and pays $10 GST to the ATO. |

| GST credit | $0 | |||||

| Net GST to pay | $10 | |||||

| Production | ; | Net GST to pay | ; | What happens | ||

| T-shirt manufacturer sells t-shirts for $220 including $20 GST | ; | GST on sale | $20 | Manufacturer pays $10 GST to ATO | ; | The T-shirt manufacturer can claim a credit for the $10 GST included in the price paid to the cotton grower. The manufacturer offsets that $10 against the $20 collected on the sale of the t-shirts to the retailer and pays $10 GST to the ATO. |

| GST credit | $10 | |||||

| Net GST to pay | $10 | |||||

| Retail distribution | ; | Net GST to pay | ; | What happens | ||

| Retailer sells T-shirts for $330 including $30 GST | ; | GST on sale | $30 | Retailer pays $10 GST to ATO | ; | The retailer can claim a credit for the $20 GST included in the price paid to the t-shirt manufacturer. The retailer offsets that $20 against the $30 GST collected on the sale of the t-shirt to the consumer and pays $10 GST to the ATO. |

| GST credit | $20 | |||||

| Net GST to pay | $10 | |||||

| Consumer retail | ; | Net GST to pay | ; | What happens | ||

| Consumer pays $330 (including $30 GST) to the retailer | ; | $30 total GST paid to ATO | ; | The consumer who buys the T-shirt bears the $30 GST included in the price, as consumers can't register for GST and cannot claim GST credits | ||

Tax codes are used to track taxes paid to a business and by a business. Each code represents a particular type of tax.

When the GST system was introduced in 2000 it was made more complex than was originally intended. The government decided to exclude some goods and services from the 10 percent tax, rather than having GST applied to all goods and services.

As a result the GST system was split into three categories of goods and services. These are:

- GST-free: no GST is collected for certain goods and services

- input taxed: used for supplies on which no GST is added to the final purchase price, such as residential rents or unit trusts

- GST taxable: most goods and services

Note: Businesses that sell or provide GST-free goods and services do not charge the 10 percent GST tax but can claim any GST input tax credits included in their costs.

As a refresher, here is a look at all of the Australian tax codes:

| Tax code | Name | Description | Default tax type |

|---|---|---|---|

| GST | Goods & Services Tax | General tax of 10% on most goods and services including bank merchant fees, and other items sold or consumed in Australia | Goods & Services Tax |

| FRE | GST-Free | Sales that are GST-free sales other than export sales, such as fresh food purchases, bank fees, medical services and products, and educational courses | Goods & Services Tax |

| EXP | Export Sales | Used when exporting goods, which are usually GST-Free | Goods & Services Tax |

| CAP | Capital Purchase | Amounts paid for capital assets, such as plant and equipment, motor vehicles, land and buildings | Goods & Services Tax |

| INP | Input Taxed Purchases | Used for the purchase of input taxed supplies, or supplies on which no GST is added to the final purchase price, such as residential rents or unit trusts | Input Taxed |

| ITS | Input Taxed Sales | Used for the sale of input taxed supplies, or supplies that don't include GST in the sale price, such as financial supplies, interest income and residential income | Goods & Services Tax |

| LCT | Luxury Car Tax | Luxury car tax (LCT) is a 33% tax on cars that have a GST-inclusive value above the LCT threshold paid by businesses that sell or import luxury cars (dealers), and by individuals who import luxury cars. | Luxury Car Tax |

| LCG | Consolidated LCT & GST | This tax code combines GST and LCT to calculate and track both taxes. | Consolidated |

| GNR | GST Not Registered | Used to record purchases from suppliers who have an ABN but are not registered to collect GST | Input Taxed |

| ABN | No ABN Withholding | Used for suppliers that have not quoted ABNs on their invoices, or for amounts that are withheld from investment income because no tax file number was quoted. | No ABN/TFN |

| N-T | No-Tax | Used to record sales that carry no GST, such as depreciation and cash transfers. | Goods & Services Tax |

| WEG | GST on Wine Equalisation Tax | Used to record GST and WET on the same invoice. However, If an invoice only contains a WEG figure and doesn't show WET and GST separately, it won't contain all of the necessary information to claim GST credits. To ensure the invoice is a "tax invoice" it must clearly show the breakdown of GST and WET. | Goods & Services Tax |

| WET | Wine Equalisation Tax |

WET is a tax of 29% of the wholesale value of wine. It is generally only payable if you are registered or required to be registered for GST. It is designed to be paid on the last wholesale sale of wine, usually between the wholesaler and retailer but is also included in cellar door or tasting room sales, where there hasn't been a wholesale sale. WET is also payable on imports of wine (whether or not you are registered for GST). |

Sales Tax |

| GW | Consolidated WEG and WET | Combines the Wine Equalisation GST (WEG) and Wine Equalisation Tax (WET) codes | Consolidated |

| VWH | Voluntary Withholdings | Used for contractor payments where a voluntary agreement is in place. | Voluntary Withholdings |

The table above can be found on MYOB's Tax Codes help centre page. You may like to bookmark it as a tax resource.

Types of supplies in relation to GST

| Type 1 | Types 2 and 3 | Type 4 | |

|---|---|---|---|

| Taxable supplies | Non-taxable supplies | Out-of-scope supplies | |

| GST-free supplies (division 38) of ANTS Act 1999 (Cth) | Input Taxed Supplies (Division 40) of ANTS Act 1999 (Cth) | ||

| Definition | |||

| Goods and services sold or purchased by a business. An entity us required to charge 10% GST on all "taxable supplies". |

GST-free supplies are those which the Act does not require GST to be charged on | Input Taxed supplies are those which the Act doesn't require GST to be charged on | These supplies are not goods or services - they are outside the scope of the GST Act. Including items which do not include consideration. |

| Examples | |||

|

|

The following may be elected as input taxed:

|

|

*Check the ATO website for current limits for the financial year

Activities: Understanding and applying GST

- Take five minutes to watch the video on the Goods and services tax (GST) page on the ATO website to help you understand:

- how GST works

- when you have to register

- what you have to do when you are registered for GST.

- Take this quiz about GST codes

Types of sales

Review the list below to review the types of sales and their GST requirements.

Taxable sales35

You must pay GST on taxable sales that you make. To be a taxable sale (that is, a sale that has GST in the price), a sale must be the following:

Sales for payment

For a sale to be taxable, it must be made for payment. This is usually monetary, but can be some other form of payment, such as the following:

Sales in the course of operating your business

This usually means that you provide the goods or services while conducting your business. It includes all sales of business assets, including items such as motor vehicles and office plant and equipment. It also includes tasks done when setting up or winding down your business.

Sales connected with Australia35

A sale of goods is connected with Australia if the goods are:

- delivered or made available in Australia to the purchaser;

- removed from Australia, or

- brought to Australia, provided the seller either imports the goods into Australia or installs or assembles the goods in Australia.

The sale of a property is connected with Australia if the property is in Australia. for GST purposes, property includes the following:

- land

- land and buildings

- interest in land

- rights over land

- a licence to occupy land.

A sale of something other than goods or property is connected with Australia if the:

- the thing is done in Australia

or - the seller makes the sale through a business they carry on in Australia

or - the sale is of a right to purchase something that would be connected with Australia.

You pay GST on the taxable sales you make when you lodge your activity statement.

For these taxable sales, you:

- include GST in the price

- issue a tax invoice to the buyer

- pay the GST you’ve collected when you lodge your activity statement.

Partly taxable sales35

If your sale can be separated into identifiable parts and any of those parts are GST-free or input-taxed, the sale is partly taxable. You only need to pay GST on the taxable part of the sale.

Capital assets35

Sales of business assets, such as office equipment and motor vehicles, are usually taxable sales. GST also applies to business assets you trade-in or otherwise dispose of by transferring ownership.

Input-taxed sales

Input-taxed sales are sales of goods and services that don’t include GST in the price. You can’t claim GST credits for the GST included in the price of your “inputs”.

The most common input-taxed sales are the following:

Financial supplies

You generally make a financial supply when you:

- lend or borrow money;

- grant credit to a customer;

- buy or sell shares or other securities;

- create, transfer, assign, or receive an interest in, or a right under, a superannuation fund; or

- provide or receive credit under a hire purchase agreement if the credit is provided for a separate charge that is disclosed to the purchaser.

In special cases, you may be entitled to claim a GST credit for a purchase that relates to making a financial supply if:

- you do not exceed the financial acquisitions threshold

or - your purchase relates to an amount you borrowed and used to make a non-input taxed sale

or - your purchase qualifies as a reduced credit acquisition – you will be entitled to a reduced GST credit.

Grants and Sponsorship

- Grants: If your organisation is registered for GST – or required to be – and receives grant funding (from a government body or private foundation, for example), it may not have to pay GST on the funding payment unless it makes a “supply” in return for the payment.

- Sponsorship: Under a sponsorship arrangement, when an organisation undertakes a fundraising activity, it often receives support in the form of money. In return, it may provide such things as advertising, signage, naming rights, or some other type of benefit of value.

- This means that the sponsor receives something of value in return for the sponsorship, so the sponsorship payment is not a gift.

- If the organisation is registered for GST, it has to pay GST on the sponsorship it receives. On the other hand, the sponsor may be able to claim a GST credit.

Insurance settlements

You do not have to pay GST on an insurance settlement, provided you tell the insurer before making the claim what proportion of the premium you can claim GST credits for. (You can claim GST credits on the part of the premium related to business purposes.)

If you do not tell your insurer before making the claim, you may have to pay GST when your claim is settled and you lodge an activity statement.

The insurer will expect to cover you only for the actual loss – that is, the loss minus the amount of GST credits you can claim on the repair or replacement cost of the item insured.

GST-FREE supplies

You do not include GST in the price if your product or service is GST-free, but you can still claim credits for the GST included in the price of purchases you use to make your GST-free sales.

In principle, most basic foods, some education courses, some medical products, and health and care services are exempt from GST.

There are some exceptions within these categories, but generally, GST-free includes:

The following links to the ATO provide additional detail.

For food, refer to:

- The GST food guide (NAT 3338), which contains an alphabetical list showing whether general food and drink products are taxable or GST-free

- GSTD 2002/2 Goods and services tax: what supplies of fruit and vegetable juices are GST-free.

For health, refer to GST and:

- medical services

- other health service

- medical aids and appliances

- Herbal medicine practitioners and naturopaths

- Certificate for medical assessment to obtain a car or car parts GST-free (NAT 3417)

The following relates to education and charities regarding GST. Take some time to research information about these areas:

For education, refer to:

- GST for preschool operators (NAT 12579).

- GSTR 2000/27 Goods and services tax: adult and community education courses; meaning of “likely to add to employment related skills”.

- GSTR 2000/30 Goods and services tax: supplies that are GST-free for pre-school, primary, and secondary education courses.

- GSTR 2001/1 Goods and services tax: supplies that are GST-free for tertiary education courses.

- GSTR 2002/1 Goods and services tax: supplies that are GST-free as special education courses.

- GSTR 2003/1 Goods and services tax: supplies that are GST-free as professional or trade courses.

- GSTD 2000/11 Goods and services tax: is the supply of commercial pilot training GST-free as an education course under section 38-85 of the New Tax System (Goods and Services Tax) Act 1999 (Cth) (the GST Act).

- GSTD 2000/7 Goods and services tax: is the supply of the services of apprentices or trainees by a Group Training Company to host employers under a Group Training Scheme a taxable supply in terms of section 9-5 of the New Tax System (Goods and Services Tax) Act 1999 (Cth).

For non-commercial activities of charities, refer to:

- GST and fundraising dinners or similar functions;

- endorsements to access charity tax concessions;

- Fundraising (NAT 13095);

- Tax basics for non-profit organisations (NAT 7966);

- Volunteers and tax (NAT 4612).

Registration and turnover

- As a reminder, a business can only register for GST if it has an Australian Business Number (ABN).

- Your ABN will also be your GST registration number.

What businesses need to apply?

Greater than $75,000

- If you run a business or other enterprise and have a GST turnover of $75,000 or more ($150,000 or more for non-profit organisations) or you expect to do so if it is your first year of operation.

or - You provide taxi travel (including ride-sourcing) as part of your business, regardless of your GST turnover. (Taxi travel means transporting passengers by taxi or limousine for fares.)

Less than $75,000

- If you carry on a business but have a GST turnover of less than $75,000 (or $150,000 for non-profit organisations), you can choose to register for GST.

- Having a turnover of less than $75,000 in this context gives you the option to calculate, report and pay your GST annually. Generally, you must then stay registered for at least 12 months.

- If you are not registered for GST, you must check monthly to see whether you have reached the GST turnover threshold. If you reach the threshold, you must register for GST within 21 days.

Working out GST turnover

The GST turnover is your gross business income (not your profit), excluding any

- GST you included in sales to your customers

- Sales that are not for payment and are not taxable

- Sales not connected with an enterprise you run

- Input-taxed sales you make

- Sales not connected with Australia.

Note: GST, input taxed supplies, supplies not taxable, and supplies not connected with the enterprise are not included in the calculation.

You reach the GST turnover threshold if either:

- Your turnover for the current month and the previous 11 months is $75,000 or more ($150,000 for non-profits.) = Current GST turnover.

or - Your turnover for the current month and the next 11 months is likely to be $75,000 or more ($150,000 for non-profits.) = Projected GST turnover.

One owner for multiple businesses

- If a business owner has more than one business, they can only register once for GST.

What happens if a business doesn't comply?

- If a business is not registered but is required to do so, it has to pay GST on the sales it has made since the date it was required to register together with penalties and interest.

Closing the business - selling off business assets

In working out your projected GST turnover, you do not include amounts you received for the sale of a business asset (such as the sales of a capital asset) or for any sale you made, or are likely to make, solely as a consequence of ceasing or substantially and permanently reducing the size of your business.

GST Groups and Branches

A GST group is two or more associated business entities that operate as a single business for GST purposes and satisfy certain membership requirements.

- One group member (the “representative member”) completes activity statements and accounts for GST on behalf of the whole group.

- If you are a member of a GST group, your turnover includes the turnover of the other group members (except supplies made from one member of the group to another member of the group).

- GST groups are treated as a single entity. Generally, transactions between group members are ignored for GST purposes. So you don’t have to pay GST, and you can’t claim GST credits on these transactions.

A GST branch is formed when a business entity separately registers its branch to suit the structural, management, and accounting arrangements of the organisation. When an entity registers a branch for GST purposes, the entity is called the “parent entity”.

- A GST branch accounts for GST separately from their parent entity.

- If an entity registers a branch for GST purposes, the branch operates as a distinct entity for reporting purposes, accounting for GST separately from its parent entity.

- Unlike GST groups, transactions between the branch and the parent entity will be taxable, and GST credits can be claimed.

GST Simplified Accounting Methods (SAM) for Food Retailers

Many small food retailers buy and sell products that require GST (such as prepared food), as well as products that are GST-free (such as fruits and vegetables). Others buy products requiring GST (imported, sweet mango chutney) and GST-Free products (bread, lettuce, tomato, ham) but sell only GST products (sandwiches).

Depending on the point-of-sale equipment they use, accurately identifying and recording GST-free sales separately from those that are taxable can be difficult, which makes accounting for GST complicated.

The Simplified GST accounting methods for food retailers was introduced by the ATO to make it easier to account for GST. These methods will help the small food retailer work out the amount of GST they are liable to pay at the end of each tax period. We have provided the link, but please note that you could have found this information on the ATO by searching for "NAT 3185".

There are five methods to choose from, so you need to decide which one is best for your business:

- Business norms

- Stock purchases

- Snapshot

- Sales percentage

- Purchases snapshot

| Method | Business Norms | Stock Purchases | Snapshot | Sales Percentage | Purchase snapshot |

|---|---|---|---|---|---|

| Turnover threshold | SAM* turnover of $2millon or less | SAM* turnover of $2millon or less | SAM* turnover of $2millon or less | GST turnover of $2million or less | GST turnover of $2million or less |

| How GST-free sales 7/or purchases is estimated | Apply standard percentages to sales and purchases | Use a sample of purchases | Use a snapshot of sales and purchases | Use percentage of GST-free sales made in a specified tax period and apply this to purchases | Use a snapshot of purchases to calculate GST credits |

*Simplified Accounting Methods (SAM)

Note: The averaging involved in these methods cannot be used to set your prices – you need to keep doing this in line with the Australian Competition and Consumer Commission’s (ACCC) guidelines.

Example of the Business Norms method

The Business norms method is the simplest way to work out your GST. This method can be used if all of the following conditions are met.

- Available to specified business types only listed in the Business norms table and pharmacies that sell food and rural convenience stores.

- Nature of business – reseller and/or converter.

- Point-of-sale equipment – inadequate.

- Same premises – sell taxable and GST-free food on the same premises.

- Turnover threshold – SAM turnover of $2 million or less.

| Type of retailer | Percentage for GST-free sales | Percentage for GST-free trading stock purchases |

|---|---|---|

| Cake shop | 2% | 95% |

| Continental delicatessen | 85% | 90% |

| Convenience store that prepares takeaway food | 22.5% | 30% |

| Convenience store that doesn't prepares takeaway food | 30% | 30% |

| Fresh fish shop | 35% | 98% |

| Health food shop | 35% | 35% |

| Hot bread shops | 50% | 75% |

| Pharmacies that also sell food | Dispensary non-claimable 98% | Nil |

| Over-the-counter 47.5% | 2% | |

| Rural convenience stores | Converters: 22.5% | 30% |

| Non-converters: 30% | 30% |

Activity:

The ATO has definitions for each type of the five types of retailer, we've just shown one — the Business Norms Method.

See if you can find information about each of them on their website.

Keep up with the ATO's changes to GST applied to food

Staying on top of changes to these laws is important so a business knows whether a product has moved from GST to GST-Free or vice versa. The ATO provides this page to track and communicate those changes: Goods and Services Tax Industry Issues Detailed Food List.

General accounting methods - a refresher

There are two methods of accounting for GST: Cash Basis and Non-Cash Basis (accruals). The method you use will affect when you will report GST.

You will likely be familiar with accounting methods, but here is a refresher on the information about cash vs accrual based, and double-entry accounting, which will assist with your understanding of GST calculations.

Cash vs Accrual based accounting

Revenue and expenses can be recorded on either a cash or accrual basis and the difference between them focuses on when transactions are recorded vs occurred in real life..

With cash accounting:

- Revenue is recorded when the cash is received from the customer

- Expenses are recorded when the cash is paid

With accrual accounting:

- Revenue is recognised in the period it is which the revenue is earned

- Expenses are recognised in the period they are incurred

| June | July | |||

|---|---|---|---|---|

| Activity | Purchase parts, repair car, pay employees, receive payment for work done in June. | |||

| Accrual Basis | Revenue | $3,000.00 | Revenue | $0.00 |

| Expense | $1,800.00 | Expense | $0.00 | |

| Profit | $1200.00 | Profit | $0.00 | |

| Cash Basis | Revenue | $ - | Revenue | $3,000.00 |

| Expense | $1,800.00 | Expense | $0.00 | |

| Profit | -$1,800 | Profit | $3,000.00 | |

How cash or accrual basis affects GST reporting

The table below summarises the differences between the two methods of accounting for GST.

| Cash basis | Non-cash basis | |

|---|---|---|

| Used by | Small businesses | Most large businesses |

| Turnover | Less than $2 million | More than $2 million |

| Advantage | Money flowing to the business is better aligned with the activity statement liabilities | |

| GST | GST on the BAS covers the period in which the sales or purchases are collected and paid respectively | GST on the BAS covers teh period in which the tax invoice is issued or received |

| Sales | GST payable on the sales is accounted for in the reporting period their payment is received. In case you only received part payment for a sale in a reporting period, you only account for the GST for the part of the payment you received. | GST payable on the sales is accounted for in the reporting period in which a tax invoice is issued or payment is received in full or partial, whichever happens first. |

| Purchases | GST credits can only be claimed with a tax invoice, except for purchases costing $82.50 or less. *you have 4 years to claim credits |

GST credits can only be claimed with a tax invoice, except for purchases costing $82.50 or less. *you have 4 years to claim credits |

Videos

If you struggle with the concepts, the following two videos offer an engaging way to understand cash vs accrual:

Cash accounting:

Accrual-based accounting:

Double-entry Bookkeeping system

Double-entry bookkeeping is an accounting method that keeps a company's accounts balanced and provides an accurate financial picture of a company's finances. In double-entry bookkeeping for every debit, there must be a corresponding credit.

The double-entry method of bookkeeping records transactions based on the principle of duality; that is, for each debit entry in the ledger, there is a corresponding credit entry. It fully records the effects of every transaction in the accounts in the chart of accounts, making reconciliation possible, and agrees with Generally Accepted Accounting Principles (GAAP). It is the method most businesses adopt.

Double-entry bookkeeping relies on the accounting equation to ensure that the accounts are always balanced. Take a minute to remind yourself by putting the phrase together in this short activity.

Invoicing, or providing a receipt or sales docket is a way of recording and reporting for tax and GST requirements.

Rules for invoices

- If the taxable sale amounts to more than $82.50 (including GST), the GST-registered customers must be given a tax invoice so that the business can claim a credit for the GST in the purchase price.

- If a customer or client asks the seller for a tax invoice, they must provide one. They must be registered for GST to issue a tax invoice.

- If the sale is over $1000:

- Tax invoices for sales of $1,000 or more also need to show the buyer's identity or ABN.

- If your tax invoices meet the requirements for sales of $1,000 or more, you can also use them for sales of lesser amounts.

- If the sale has both taxable and non-taxable items, the tax invoice must also show:

- each taxable sale

- the amount of GST to be paid

- the total amount to be paid.

- If the supplier does not provide an ABN and the total payment for goods and services is more than $75 (excluding GST) you generally withhold the top rate of tax from the payment and pay it to us.

Under normal circumstances, a receipt, docket, or invoice must have a certain amount of information for it to be a valid tax invoice. It must include the following:

- the words tax invoice stated prominently

- the date of issue of the tax invoice

- the name of the supplier

- the supplier’s Australian Business Number (ABN)

- the GST-inclusive price of the taxable supply

- when GST is exactly one-eleventh of the total price, a statement that GST has been included within the total price charged

- an indication of which items represent taxable sales and which do not, if any

- a brief description of each thing supplied

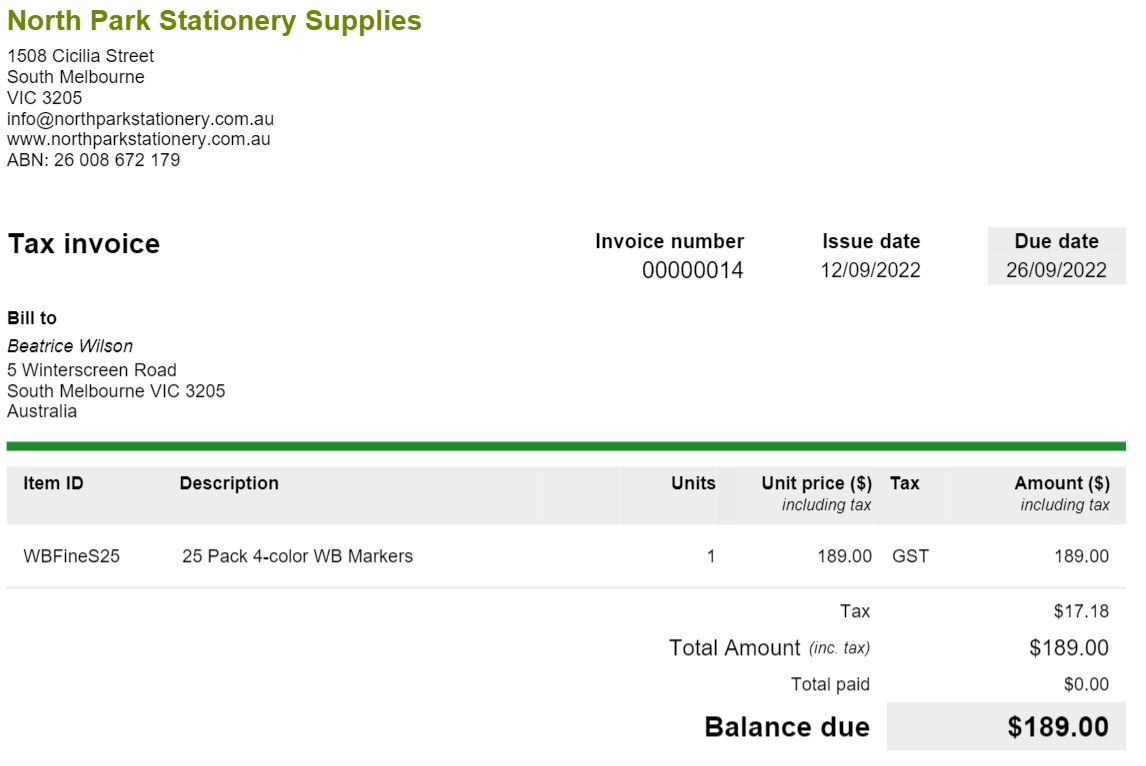

The invoice below was generated in MYOB. See if you can find all of the elements from the list above reflected on it.

Did you find everything? 'The Total Amount (inc. tax)' let's the ATO and customer know that the total amount on the invoice is a GST inclusive amount.

Take a look at this excellent resource from the ATO about Tax invoices.

Digital invoices

A tax invoice doesn't need to be issued in paper form. The record transmitted to the customer needs to contain all information required for a tax invoice.

For example, you can issue a tax invoice to a customer by:

- using eInvoicing (Peppol eInvoice), an automated direct exchange of invoices between a supplier's and buyer's software, or

- emailing an invoice in portable document format (PDF)

MYOB Business accounting software makes invoicing easy with PDF invoicing and online payments.

GST Calculator

The Australian government provides a link to a GST calculator so that suppliers can determine GST obligations and credits. It helps businesses ensure they are charging the correct GST.

- How to calculate GST (goods and services tax) in Australia

- The amount of GST you will pay or should charge customers

- The price excluding GST and the total cost including GST

Reading

Use MYOB or Xero for GST Reporting

To find out more about GST Reporting using MYOB or Xero please access the links below:

You can claim a credit for any GST included in the price of any goods and services you buy for your business.

Paying GST for an item you sell, or use in the production of the item you sell is called a GST credit; or an input tax credit – a credit for the tax included in the price of your business inputs.

Your business can claim GST credits if the following conditions apply:

- The business is registered for GST.

- The taxed purchase was made within the last four years.

- The purchase was intended to be used solely or partly in carrying on the business, and the purchase does not relate to making input-taxed supplies.

- The purchase price included GST.

- You provide or are liable to pay for the item you purchased.

- You have a tax invoice from your supplier (for purchases more than $82.50).

To calculate the amount of GST that has been included in the price of a purchase using the following formula:

The GST inclusive price of the good or service × 1/11 = the GST included in the price of the purchase

You cannot claim a GST credit:

- without a valid tax invoice

- for purchases that do not have GST in the price

- for wages you pay to staff (there is no GST on wages)

- for motor vehicles priced above a certain limit.

Goods and services that do not have GST in their price include:

- GST-free items (such as basic foods)

- input-taxed items (such as bank fees and loan interest)

- purchases from a business that is not registered for GST (and therefore cannot charge GST).

You also cannot claim GST credits for the following, even if GST is included in the price:

- purchases you intend to use for private or domestic purposes

- purchases you intend to use to make input-taxed supplies, such as those associated with providing residential accommodation

- some purchases that you can’t claim as an income tax deduction, such as entertainment expenses

- land purchases under the margin scheme.

GST credits and income tax deductions

If you can claim a deduction for a business purchase in your income tax return, claim the amount of the purchase on the income tax statement less any GST credit, which is reported on the BAS.

For example: Roberta, a tax agent, purchased stationery for her business. She pays $55 for the stationery, which included $5 for GST. Roberta can claim a GST credit of $5 on her BAS and $50.00 as an income tax deduction on his income tax return.

If you are not entitled to a GST credit, claim the full cost of the purchase, including any GST, as a deduction.

For example: Leonard is a BAS agent, and is not required to be registered for GST as he doesn't sell taxable goods or services. He will claim the full cost, $55 (including GST), as a deduction.

For capital items, such as machinery, you may be entitled to an income tax deduction for the item’s decline in value (depreciation). When working out the decline in value, use the cost of the item less any GST credits you are entitled to.

For example: Lila is registered for GST and buys a new printer for her business. The seller is registered for GST and charges Lila $1100 (including $100 GST). Lila can claim a GST credit of $100 on her activity statement, and she can claim an amount that reflects the decline in value of the printer on her income tax return. Lila subtracts her GST credit from the purchase price (that is, $1100 - $100 GST = $1000), and uses $1000 to calculate her depreciation.

Credits don't last forever

See the ATO for more information about time limits on GST credits and refunds.

The resources and activities here will help confirm your understanding of the GST system.

Resource: This pamphlet, published by the ATO, is a quick, handy guide to the main points of the GST system of taxation.

Resource: The ATO's Detailed Food List provides a thorough look at GST for edible items. Have a look at it before moving on to the next two activities.

Scenario:

Activity: Take this five question quiz