This section covers the regulations governing BAS agents and activities, and tax legislation and reporting.

The ATO requires that businesses lodge business activity statements as a tax reporting requirement on either a monthly, quarterly, or annual basis. They are used to report and pay a business’s GST and PAYG withholding liabilities for the period. They will also include PAYG income tax instalments and fringe benefits tax instalments where necessary.

Understanding Business Activity Statements

There are two types of activity statements – an instalment activity statement (IAS) and a business activity statement (BAS). The IAS is the simpler of the two forms and is only issued quarterly.

Instalment Activity Statement (IAS)

The only tax obligations reported on the IAS are pay as you go (PAYG) instalments and PAYG withholding tax. The goods and services tax (GST) is not included on the IAS since it’s only reported on the BAS.

On the IAS, the ATO informs you what your GST instalment amount is and, where applicable, what your PAYG instalment amount is.

There is no need to print any reports from your accounting software or make any calculations. However, there are benefits if you can accurately calculate your liability.10

Suppose the ATO considers you to be eligible for the IAS system. In that case, you will have the option of using the simpler of activity statements on your September BAS – the first BAS of the financial year. If you decide to use this option, for each of the next three-quarters, you will simply be sent an amount that needs to be paid to the ATO.

If you feel the instalments advised are too much or not enough to cover your liabilities, you may vary the amounts paid. Alternatively, you can wait until the end of the year. Any adjustments to GST will be calculated when your annual GST return is lodged. Any adjustments to PAYG will result in an amount payable or refundable when your income tax return is lodged.

If you choose to pay the amount shown on the form, you do not need to lodge anything with the ATO. However, if you wish to vary the amount shown, you will need to lodge the form by the due date.11

This system allows businesses to pay accrued liabilities throughout the year instead of incurring large expenses all at once at the end of the financial year. When a business registers for an Australian business number (ABN) and GST, the ATO will automatically send a BAS when it is time to lodge.

All businesses registered for GST are required to lodge a BAS or IAS by their due dates.

The instalment amounts payable as follows:

| Quarter it covers | Due |

|---|---|

| July-September | 28 October |

| October-December | 28 February |

| January-March | 28 April |

| April-June | 28 July |

You are required to lodge an IAS if you are a medium withholder. You are considered a medium withholder if you are an individual or business that withholds $25,001 up to $1 million from your employees’ salaries.

The Business Activity Statement (BAS)

The New Tax System mandates that businesses registered for GST would report their tax obligations and entitlements on a single compliance form called the Business Activity Statement (BAS) issued by the ATO. It is an “activity” statement and, as such, more than just tax figures are reported.

How much do you already know?

Before we continue, test the knowledge you have already learned about what the BAS is used for.

How much did you remember?

The BAS is used to report and pay13:

GST is a value-added tax of 10% on most goods and services. Some exemptions apply to certain businesses. You can use your BAS to report, record and pay the GST your business has collected and claim GST credits. Your business can claim GST credits at any time within four years from when you meet the relevant requirements. We'll provide more information about GST credits later in this topic.

For GST purposes, each BAS covers a ‘tax period’ (one or three months). However, the BAS form is used for all tax payments, including fringe benefits tax and PAYG.

PAYG instalments require you to pay incremental amounts towards your expected end of year income tax liability. You can choose between an instalment amount (such as $15,950.00) or an instalment rate (such as 8%). The ATO works out an instalment amount based on the information you reported in your most recent tax return. An instalment rate is worked out by the business itself based on actual income as it is earned.

The ATO generally sends PAYG instalments in the form of an instalment notice rather than a BAS.

Separate from income tax, fringe benefits tax (FBT) is a tax that employers pay on certain benefits they provide to their employees, including their employees’ family or other associates on behalf of the employee. These benefits include allowing employees to use their work vehicle for private purposes or paying an employee’s gym membership. If a business was required to pay FBT of $3,000 or more in a preceding financial year, it must include this in its BAS and pay quarterly.

The luxury car tax (LCT) applies to all supplies and importations of luxury cars where the value (including GST) exceeds the LCT threshold. The ATO determines this threshold and is subject change to change. At the time of writing, LCT is at 33% and applies to the portion of the car’s value above the threshold, not the car’s total value.

In some circumstances, you may be able to defer paying LCT if you meet specific criteria determined by the ATO. This may include if you plan to use the car to:

- hold it for trading stock (not including holding it for hire or lease);

- carry out research and development for the car’s manufacturer, or

- export it GST-free.

The WET only applies to wine manufacturers, wholesalers and importers, and is a tax based on the value of wine. At the time of writing, the WET is at 29% of the taxable value of wine.

If you report and pay GST annually, you are not required to report WET on a monthly or quarterly BAS. However, you must report WET on your annual GST return.

Fuel tax credits provide businesses with a credit for the fuel tax (excise or customs duty) included in the fuel price they use in machinery, plant equipment and heavy vehicles for business purposes. The FTC rates vary from time to time. Therefore, it is essential to check with the ATO for the current rates at any time that a business wishes to make such a claim.

The credit amount depends on:

- when you acquire the fuel;

- what fuel you use; and

- the activity you use it in.

For context, here is a look at all of the Australian tax codes:

| Tax code | Name | Description | Default tax type |

|---|---|---|---|

| GST | Goods & Services Tax | General tax of 10% on most goods and services including bank merchant fees, and other items sold or consumed in Australia | Goods & Services Tax |

| FRE | GST-Free | Sales that are GST-free sales other than export sales, such as fresh food purchases, bank fees, medical services, health, and care services and products, and educational courses | Goods & Services Tax |

| EXP | Export Sales | Used when exporting goods, which are usually GST-Free | Goods & Services Tax |

| CAP | Capital Purchase | Amounts paid for capital assets, such as plant and equipment, motor vehicles, land and buildings | Goods & Services Tax |

| INP | Input Taxed Purchases | Used for the purchase of input taxed supplies, or supplies on which no GST is added to the final purchase price, such as residential rents or unit trusts | Input Taxed |

| ITS | Input Taxed Sales | Used for the sale of input taxed supplies, or supplies that don't include GST in the sale price, such as financial supplies, interest income and residential income | Goods & Services Tax |

| LCT | Luxury Car Tax | Used to handle special tax considerations which accompany the sale of luxury cars | Luxury Car Tax |

| LCG | Consolidated LCT & GST | This tax code combines GST and LCT to calculate and track both taxes. | Consolidated |

| GNR | GST Not Registered | Used to record purchases from suppliers who have an ABN but are not registered to collect GST | Input Taxed |

| ABN | No ABN Withholding | Used for suppliers that have not quoted ABNs on their invoices, or for amounts that are withheld from investment income because no tax file number was quoted. | No ABN/TFN |

| N-T | No-Tax | Used to record sales that carry no GST, such as depreciation and cash transfers. | Goods & Services Tax |

| WEG | GST on Wine Equalisation Tax | Used to record GST on WET | Goods & Services Tax |

| WET | Wine Equalisation Tax | Tax on wine consumed in Australia based on the value of the wine | Sales Tax |

| GW | Consolidated WEG and WET | Combines the Wine Equalisation GST (WEG) and Wine Equalisation Tax (WET) codes | Consolidated |

| VWH | Voluntary Withholdings | Used for contractor payments where a voluntary agreement is in place. | Voluntary Withholdings |

The table above can be found on MYOB's Tax Codes help centre page. You may like to bookmark it as a tax resource.

Download a blank sample BAS statement

Download this sample BAS statement, and review the sections and fields. We'll provide more information about how to complete them later in the course.

Simpler BAS

Since 1 July 2017, Simpler BAS is the default reporting method for small businesses with a GST turnover of less than $10 million.

Small businesses only need to report:

- Total sales;

- GST on sales;

- GST on purchases.

The following GST information is no longer required:

- Export sales

- GST-free sales

- Capital purchases

- Non-capital purchases.

Simpler BAS does not affect how other taxes are reported (e.g. PAYG income tax instalments or PAYG tax withheld) or how often you lodge your BAS. You still need to keep records, such as tax invoices, as proof of any claims you make in your BAS and income tax return lodgments.12

The ATO developed the Simpler BAS GST bookkeeping guide to what is and is not included in a BAS. Before continuing, please read through this useful page. You may like to bookmark it for future reference. The information will be useful while completing your assessments.

Due dates and requirements of lodging BAS and IAS

The BAS is created for each business in Australia and sent by the ATO either monthly or quarterly. The form needs to be lodged with the ATO and payment made according to the following due dates:

- For monthly BASs – within 21 days of the end of the month on the form, and

- For quarterly BASs – as for IASs (see above).

Businesses and entities registered for GST are required to lodge a BAS. Businesses not registered for GST must lodge an IAS, which is used for reporting only PAYG (withholding), PAYG (instalments), FBT.

The ATO sends forms via the post or electronically. If you do not receive a form, contact the ATO before your normal due date. Businesses must use the form provided as these forms are preprinted and personalised with the following information.

- Each BAS has a unique Document Identifier Number (DIN) and barcode. A business’s PAYG instalment rate and FBT instalment obligation also appear on the form.

- Each BAS has preprinted information regarding when the BAS must be lodged and the period covered for each obligation.

Payment and lodgment of the BAS

- For GST purposes, each BAS covers a “tax period” (one or three months). However, the BAS form is used for all tax payments, such as FBT, PAYG withholdings, etc.

- These tax payments may be payable at different times to GST (e.g. PAYG is monthly). Therefore, the BAS lodgment requirement depends on a business’s “status” for a number of taxes, not just GST.

- Generally, payment and lodgment of the BAS is within 28 days following the end of the reporting period. (The dates are preprinted on the BAS form).

- BAS lodgment can be made electronically or by post using the pre-addressed envelope provided by the ATO (all lodgment must be made using the official BAS form).

Legislation and regulations

In Australia, agents providing BAS and/or Tax services must be registered with the ATO, which is bound by various tax legislation.

The tax agent services legislation consists of:

- Tax Agent Services Act 2009 and Regulations and amendments

- Tax Agent Services (Specified BAS Services) Instrument 2016

Other legislation that relates to taxation includes:

- Taxation Administration Act 1953

- Corporations Act 2001

- Criminal Code Act 1995

- Freedom of Information Act 1982

- Privacy Act 1988

- Income Tax Assessment Act 1997

- Originally written in 1936, significant changes were made to it in 1997

- The term ‘BAS provision’ is defined in the Income Tax Assessment Act 1997 as:

- Part VII (collection and recovery only) of the Fringe Benefits Tax Assessment Act 1986

- the indirect tax laws, including

- the goods and services tax (GST) law

- the wine tax law

- the luxury car tax law

- the fuel tax law, and

- Parts 2-5 and 2-10 in schedule 1 of the Tax Administration Act 1953, which are about the pay as you go (PAYG) system

- Goods and services tax Act 1999

Tax reporting requirements for a business include:

- Payroll reporting

- Monthly or quarterly business activity statements

- Financial year reporting (1st July to 30th June)

An income tax return must be lodged by a business each year so that income and claim deductions are reported. Further lodgments of yearly reports or returns may also be required depending on whether a business is registered for other tax types.

Reports and returns can include:

- Income tax return

- PAYG withholding annual report

- GST annual return

- Taxable payments annual report (TPAR)

Each reporting function has penalty-enforced due dates and methods for lodging and payments, which will be covered in this module.

Organisational and industry requirements for lodging BAS

A business will have organisational requirements related to its tax and reporting obligations. To ensure that they are meeting all legislative compliance this information can be communicated through policies and procedures, business plans and any internal controls. For example, ensuring deadlines for BAS reporting are met or adhering to the Privacy Act for the confidentiality of client information.

It is also important for a business to find out what registrations apply to ensure that they are compliant with Australian regulations. Watch this video on the ATO website for an explanation of how to work out which registrations you need.

All businesses registered for GST are required to lodge a BAS statement to complete their GST returns. GST is mandatory for sole traders and companies with an annual GST turnover of $75,000 and above.

Registration is also required for:

- non-profit organisations with a GST turnover of $150,000 and above

- businesses/enterprises providing taxi or limousine travel for a fare as part of the business, regardless of the GST turnover. This applies to both owners drivers and those who lease or rent a taxi.

- owners wanting to claim fuel tax credits for their business/enterprise

- businesses, even if it did not earn any income or did not pay any expenses for the defined period.

Notes:

- Registering for GST is optional if your business’s annual revenue falls below the threshold or doesn’t fit into one of the categories above.

- Those not registered for GST and are not required to can submit the alternative Instalment Activity Statement (IAS).

BAS lodging with MYOB Business

When it's time to prepare the BAS or IAS, MYOB saves time by using the information in MYOB to fill in some of the details. Once you’ve filled in the other required fields on your statement, you can lodge your activity statement online and get confirmation from the ATO within seconds.

You can still complete and lodge your activity statements manually, you just need to run the GST return report for the period (Reporting menu > Reports > GST return).

Before you can lodge your activity statements online, you need to:

- have already nominated MYOB as your software provider

- set up your activity statement fields.

Further detail will be provided about using MYOB to prepare and lodge the BAS and IAS.

From 1 January 2010, a then-new regulatory regime for tax practitioners came into being, which includes the tax agent services legislative package consisting of the following:

- Tax Agent Services Act 2009 (Cth) (TASA 2009) – the main Act of which established the Tax Practitioners Board, which provides for the registration of tax agents and BAS agents.

- Tax Agent Services Regulations 2009 (TAS Regulations 2009), which contain, among other things, the following:

- The qualifications and relevant experience requirements for registration;

- The application fees for registration as a tax agent and BAS agent, and

- The requirements for recognition as a Recognised Professional Association (RPA) and BAS Agent Association.

- Tax Agent Services (Transitional and Consequential Amendments) Bill 2009 (Transitional Bill), which deals with the consequential and transitional matters arising from the enactment of the TASA 2009, including the following:

- It provides transitional arrangements that allow tax agents and nominees registered under the current law to transition smoothly into the new regulatory regime, and

- Allow certain entities to be taken as registered BAS agents under the new regime.14

The above legislative package replaced the existing rules under Part VIIA of the Income Tax Assessment Act 1936 (Cth) (ITAA 1936) and Part 9 of the Income Tax Regulations 1997.

Tax Practitioners Board (TPB)15

The Tax Practitioners Board (TPB) is a national body responsible for the registration and regulation of tax agents, BAS agents and tax (financial) advisers (collectively referred to as “tax practitioners”). The TPB is also responsible for ensuring compliance with the Tax Agent Services Act 2009 (Cth) (TASA), including the Code of Professional Conduct (Code).

This is achieved by:

- administering a system for the registration of tax practitioners, ensuring they have the necessary competence and personal attributes

- issuing guidance on relevant matters, including in regard to the Code and other identified priorities, to assist tax practitioners in providing their important service to the community

- investigating conduct that may breach the TASA, including non-compliance with the Code, and breaches of the civil penalty provisions, and

- where appropriate, applying sanctions to registered tax practitioners for non-compliance with the Code.

Note: Within this Charter the use of the Tax Practitioners Board or TPB is used to refer to the body as a whole. The use of the term ‘Board’ refers to the Board (consisting of the Board Chair and Board Members) which is responsible for making decisions on the administration of the TASA.

The Board is comprised of eight members, including the Board Chair, who are appointed for a specific period of time by the Treasurer. Board members come from a range of backgrounds including tax agent services, the bookkeeping industry, law, academia and business.

The TPB is independent of the Australian Taxation Office (ATO). While separate, the TPB and ATO work cooperatively to strengthen community confidence in the taxation system. The TPB falls under the portfolio of The Treasury.

Requirements to be a BAS Agent

The requirements for an individual to be eligible to register as a BAS agent are set out in s 20-5(1) of the TASA 2009.

An individual must be the following:

- Over the age of 18

- A fit and proper person

- The term “fit and proper person” is clearly defined by the TPB. In deciding if an individual is a fit and proper person, the Board must be presented with evidence that:

- The individual is of good fame, integrity, and character and has not been convicted of the following offences within the past five (5) years:

- a serious taxation offence

- an offence involving fraud or dishonesty

- being a promoter of a tax exploitation scheme

- implementing a scheme that has been promoted on the basis of conformity with a product ruling in a way that is materially different

- from that described in the product ruling

- the individual has had the status of an undischarged bankrupt

- the individual has been sentenced to a term of imprisonment, or served a term of imprisonment in whole or in part16

- The individual is of good fame, integrity, and character and has not been convicted of the following offences within the past five (5) years:

- The term “fit and proper person” is clearly defined by the TPB. In deciding if an individual is a fit and proper person, the Board must be presented with evidence that:

-

Comply with the education and/or experience requirements of the Tax Regulations 2009.17

Find out more information about BAS agents and the new tax agent services regime in this PDF from the ATO.(i) Accounting Qualifications

(Sch 2, Part 2, Div 1, item 201)(ii) Membership of RPA

(Sch 2, Part 2, Div 1, item 202)(iii) Membership of recognised BAS agent association

(Sch 2, Part 2, Div 1, item 203)- Individual has been awarded at least a Certificate IV Financial Services (Accounting), or a Certificate IV Financial Services (Bookkeeping) from:

- a registered training organisation

- an equivalent institution

- Has undertaken at least 1,400 hours of relevant experience in the preceding three years.

- Individual is a voting member of an RPA

- Has undertaken at least 1,000 hours of relevant experience in the preceding three years.

- Individual is a voting member of a recognised BAS agent association

- Has undertaken at least 1,400 hours of relevant experience in the preceding three years.

- Individual has been awarded at least a Certificate IV Financial Services (Accounting), or a Certificate IV Financial Services (Bookkeeping) from:

What is relevant experience?

“Relevant experience” for a BAS agent is defined in Schedule 2, Part 2, Division 2, item 204 of the draft TAS Regulations 2009.

It means work by an individual:

- as a tax agent or BAS agent registered under the TASA 2009

- as a tax agent registered under Part VIIA of the ITAA 1936

- under the supervision and control of a tax agent or BAS agent registered under the TASA 2009

- under the supervision and control of a tax agent registered under Part VIIA of the ITAA 1936

or - of a kind approved by the Tax Practitioners Board

- in the course of which the individual’s work has included substantial involvement in one or more types of BAS services. The criteria for work by an individual “of a kind approved by the Tax Practitioners Board” will be a matter for the Board to determine once established.

-

including work other than that as a registered BAS or tax agent or under the supervision and control of a registered BAS or tax agent, provided that the individual sufficiently demonstrates that their experience includes substantial involvement in providing one or more BAS services.18

Find out more about registration as an individual BAS agent in this PDF from the ATO.

The amount of relevant experience you need to demonstrate to be eligible for registration, including renewal of registration as a BAS Agent is:

- 1,400 hours in the past four years

or - 1,000 hours in the past four years if you are a voting member of a recognised BAS or tax agent association

BAS agents will not be required to demonstrate the same degree of formal education and relevant experience as tax agents. The narrower scope of services that BAS agents may provide is a result of these lower requirements.

Partnerships and Companies

Partnerships and companies that want to be in the business of providing tax or BAS services must also seek registration, and compliance with the requirements must be demonstrated by sufficient organisational qualifications and experience (ss 20-5(2) and (3) of the TASA 2009).

A company is eligible for registration as a registered tax agent or BAS agent if it can demonstrate sufficient organisational qualifications and experience (ss 20-5(2) and (3) of the TASA 2009), as shown below.

- Each director of the company is a fit and proper person;

- The company is not under external administration;

- The company has not been convicted of a serious taxation offence or an offence involving fraud or dishonesty during the previous five years, and

- The company has:

- In the case of registration as a registered tax agent – a sufficient number of individuals, being registered tax agents, to provide tax agent services to a competent standard and to carry out supervisory arrangements, or

- In the case of registration as a registered BAS agent – a sufficient number of individuals, being registered tax agents or BAS agents, to provide BAS services to a competent standard and to carry out supervisory arrangements.19

Entities that specialise in a particular area of taxation law or that only provide a certain type of tax agent service (for example, either tax compliance work or advice rather than both) will be eligible to register, with scope to operate in their specialty.

Registering to be a tax or BAS agent

When you are ready to register as an individual, a company, or a partnership, you will need to follow the instructions on the website for the TPB.

- Individual BAS agent registration

- Company or Partnership BAS agent registration

- Individual Tax agent registration

- Company or Partnership Tax agent registration

The ATO provides a thorough (34m) video describing the steps it takes to become a registered tax or BAS agent.

Registration Renewal

If your registration is approved, you will be registered for a period of at least three years. To maintain your registration, you must renew it at least 30 days before it expires.

Watch this video from the TPB to learn tips to ensure the renewal of your registration is a smooth process. The video outlines the renewal requirements and walks you through our renewal form.

For further information about renewing your registration, refer to:

Renewing your tax agent registration

Renewing your BAS agent registration

Top tips to help you renew

As a tax or BAS agent, you need to follow the policies and procedures set out in various acts.

- Requirement of registration with the Tax Practitioners Board as a registered BAS Agent under the Tax Agent Services Act 2009 (TASA) and the Tax Agent Services Regulations 2009 (Regulations).

- Recordkeeping entries of business transactions are compliant with A New Tax System (Goods and Services Tax) Act 1999 and in line with ATO publications,

- Provides payroll services that comply with Fair Work Australia Act 2009

- Ensures confidentiality and absolute security of your information, the identity and privacy of your clients and their employees as legislated under the Privacy Act 1988

- Comply with OHS legislation when servicing clients.

- Comply with The Corporations Act 2001 (Cth) when providing bookkeeping and BAS services to companies.20

Company law in Australia is enforced by the Australian Securities and Investments Commission. Some of the topics covered by the Corporations Act 2001 (Cth) include:

- the formation of companies

- the administrative details of how companies operate

- what company records businesses need to keep

- the appointment of directors, their responsibilities, how they are to resign and their conduct in relation to the operation of the company

- defines what the law is in relation to shareholders

Familiarise yourself with the following Acts and their impact on taxation laws in Australia.

- Income Tax Assessment Act 1997 - established a framework for calculating income tax assessments.

- Taxation Administration Act 1953 - provided the administrative framework for tax laws, including the collection and recovery of income tax and other liabilities.

- Privacy Act 1988 - the collection, use and disclosure of personal information

- Tax Agent Services Act 2009 - This established the Tax Practitioners Board and provides for the registration and regulation of tax and BAS agents

Australian business number (ABN)

If you are planning to run a business enterprise, it is essential you apply for an Australian Business Number (ABN) for your business. However, the business enterprise must have a Tax File Number (TFN) before applying for an ABN.

Applying for an ABN

To apply for an ABN visit the Australian Business Register.

Not everyone is entitled to an ABN. To get an ABN, you need to be running a business or other enterprise.

For example, if you want to carry out work as a sole trader with an ABN, typically, you need to be:

- Running your own business

- Paying your own income tax and GST directly to the ATO

- Sourcing your own clients, for example, by advertising your services

- Able to delegate work to others if you choose, without approval from an “employer”

- Quoting for work, including setting or negotiating your own prices

- Invoicing for work

- Maintaining a business bank account separate from your personal account

- Paying for your own business insurance, such as public liability.21

If your application is successful

- You’ll receive your 11-digit ABN immediately.

- You can continue and apply for other business registrations, such as GST.

- Your details will be added to the Australian Business Register (ABR) – but you can request that certain details not be disclosed if there is a risk to you or your family due to the information being available on ABN Lookup and data.gov.au.

- A confirmation letter will be sent to you within 14 days showing your details of the ABR – it’s then your responsibility to keep this information up to date.

If you receive a reference number, it may mean that the ATO needs to check some details in your application, or more information is needed. The ATO aims to review your application within 20 business days and contact you if further information is needed.

If your application is unsuccessful, you'll receive a refusal number. You'll also receive a letter within 14 days confirming that your application has been refused, the reasons for the refusal and the options available to you.22

Applying for an Australian Company Number (ACN)

Each and every company in Australia is issued with a unique, nine-digit number when registered. The Australian Company Number (ACN) must be displayed on all company documents, particularly appearing on the first page of any document.

Your ABN includes your nine-digit ACN.

The ABN is used in the same places that the ACN — company documents, which are “public documents” and “eligible negotiable instruments”, including:

- all documents lodged with Australian Securities and Investment Commission (ASIC)

- statements of account, including invoices

- receipts (which are not machine-produced)

- orders for goods and services

- business letterheads

- official company notices

- cheques, promissory notes and bills of exchange

- written advertisements making a specific offer.

Payroll Legislation23

Reporting on employees to the ATO is one of the crucial activities for BAS agents.

Payroll is one of the most heavily regulated parts of the Australian business landscape. Few businesses still hand out paycheques on payday, though, as most use direct deposits. Using Single Touch Payroll means most of the reporting is done automatically.

There are so many stakeholders with an interest in payroll regulation, from federal and state governments to employers, industry bodies, unions and employees themselves. Look behind some of the elements of payroll, and you will uncover a complex web of legislation and government department involvement. Such elements include:

- how much to pay

- how much tax to deduct

- how much superannuation to pay

- working conditions

- terminations.

Some major government stakeholders that a payroll professional will frequently interact with include the Australian Taxation Office, the Tax Practitioners Board, the Fair Work Commission, and the relevant state revenue authority.

The Australian Taxation Office

The ATO is responsible for administering the pay as you go withholding system (PAYGW). It interacts with employers for the collection of PAYGW on behalf of employees. Also, it plays a vital role in the administration of superannuation reporting, the superannuation guarantee system (SG) and the superannuation guarantee charge (SGC).

The Tax Practitioners Board23

The TPB is responsible for administrating the Tax Agents Services Act 2009 (TASA). This body governs the activities of people who charge clients a fee for dealing with certain taxation obligations. It seeks to protect the consumer by ensuring that only suitably qualified and experienced practitioners acting responsibly can deal with another person’s tax obligations for a fee. PAYGW and superannuation are taxation services that the TASA covers, so payroll practitioners charging a fee for dealing with these obligations on behalf of clients must register with and be accountable to the TPB.

Fair Work Commission24

The Fair Work Commission is responsible for administering the Fair Work Act 2009, a national system with far-reaching applications affecting pay rates, hours of work, leave, discrimination, dismissal, minimum wage, conditions, payslips, reporting, and much more. Its new national modern awards system has changed pay and conditions for many and exists side-by-side (at least in a transitional sense) with the existing state awards.

Revenue Office or Office of State Revenue25

State government revenue offices collect payroll tax based on wages paid in their respective states. Collected by the state or territories’ Revenue Office or Office of State Revenue, payroll tax is levied on employers with payrolls above a certain level. The states differ in their taxing rules concerning minimum thresholds, definitions of included wages, taxing rates, and more. Efforts by the states over recent years have seen them embark on a system of harmonisation to gain uniform treatment across state lines to assist employers in dealing with their payroll tax obligations.

Record keeping and reporting26

After activity statements have been prepared, obtained or the transactions completed (whichever is later), a sole trader is required to keep a copy of their general records (activity statements and payroll records) for five years. According to the ATO, a record explains the tax and super-related transactions conducted by your business.

Storing paper records electronically

Regardless of whether you use a manual or an electronic record-keeping system, you may want to store and keep paper records electronically.

The ATO accepts the imaging of business paper records onto an electronic storage medium, as long as the electronic copies:

- are a true and clear reproduction of the original paper records

- can be retrieved and read by tax officers at all times.

You don't have to keep original paper records once they have been copied onto an electronic storage medium.

PAYG withholding records you must keep

- Wages records, including payment records

- Voluntary agreements

- Employment declarations (for employees working for you before 1 July 2000), tax file number declarations and withholding declarations

- Copies of payment summaries and payment summary statements, or electronic annual reports if applicable

- Employment termination payment records

- Records of personal services income you have attributed

- Statements by a supplier where no ABN was quoted

- Records of amounts you withheld where no ABN was quoted

- Annual reports of PAYG withholding where no ABN was quoted

The ATO's business section also provides guidance for record keeping.

Activity - Five rules of record keeping

The ATO has set out five rules for record keeping. Read them on its website before returning to answer some questions to confirm your knowledge.

BAS and IAS lodgments

Penalties can be incurred for late BAS or IAS lodgments.

The actual lodgment dates for BAS or IAS are specific to the registration type and arrangements made with the tax office. The dates are printed on the forms sent by the tax office or by digital notification.

Not surprisingly, the ATO website has extensive and specific information for BAS and Tax agents. The following is a list of items that may be lodged by a tax or BAS agent (except tax returns).

- Activity statements

- Goods and services tax

- PAYG withholding payment summary annual report

- Super guarantee charge (SGC) statement quarterly form

- Taxable payments annual report

- Income statements

- Taxable and non-taxable payroll items

- Single Touch Payroll reports (STP)

- TFN reporting for closely held trusts.

- Tax returns

For more information, visit the ATO's website about due dates for lodging and paying. And this page — for the tax agent lodgment program.

The schedule for lodging and paying for your BAS depends on your GST turnover, as shown here:

- Quarterly – if your GST turnover is less than $20 million – and we have not told you that you must report monthly.

- Monthly – if your GST turnover is $20 million or more.

- Annually – if you are voluntarily registered for GST and your GST turnover is under $75,000 ($150,000 for not-for-profit bodies).

The due date for each quarter is shown in the following table:

| Quarter it covers | Due |

|---|---|

| July-September | 28 October |

| October-December | 28 February |

| January-March | 28 April |

| April-June | 28 July |

If you think you will miss a lodgment date, you can make your case by requesting a deferral.

Lodging reports and returns27

You will need to lodge an income tax return each year to report business income and claim deductions. You may also need to lodge other yearly reports or returns if you are registered for other tax types. For example, most businesses also need to lodge business activity statements.

Due to changes the government might bring about that would render the information we provided to you about specific lodgment dates for reports and returns, it's best to gain that knowledge straight from the ATO. The linked page will provide onward links to appropriate information about:

- Income tax return

- PAYG withholding annual reports

- Fringe benefits tax return

- GST annual return

- Taxable payments annual report (TPAR)

- Business activity statements (BAS)

- If you can't lodge or pay on time

Lodging with MYOB

MYOB makes it easy to prepare and lodge your statements and provides the framework for never being late or missing a payment. Several activities are consolidated for the user while MYOB does things behind the scenes. We'll cover how MYOB Business provides these features later in the module.

At the beginning of this module, we asked you to consider how important it is to have a bookkeeper managing the financial accounts in a way that accommodates payment schedules with no surprises.

That task is part of cash flow management — an accounting practice that businesses need to do because limited cash flow can hamper the financial flexibility of a business.

Budgeting to ensure sufficient funds are available to meet statutory requirements

Budgeting for your business’s tax obligations is the same as budgeting for any other expense. You will need to work out how much tax your business has to pay and then put enough money aside to cover the tax bill when it is due. Because tax bills are often payable quarterly or yearly, they may be overlooked when you budget for more frequent bills or expenses. When the time comes to pay your business’s tax bill, you may find that the money is not there, or you may have to find extra cash because your bill is larger than you expected.

The following suggestions can help you budget for your tax:

- GST reporting

- Even if you are eligible to report your business’s GST quarterly or annually, consider reporting monthly. Monthly tax periods may suit your business if it is likely to claim a GST refund regularly. For example, if your business has a large volume of exports compared with taxable sales, or if your business is likely to be making large outlays for capital equipment. You can claim GST credits sooner if your business has monthly tax periods.

- Income tax

- Estimate your business’s income for the current financial year and its potential tax liability. Update your organisation’s projection during the year as more information on sales and expenses becomes available.

- Record keeping software

- There are a number of commercially available products to help you budget for your tax. To find commercially available software that will assist you in meeting your tax obligations, visit Top 10 Accounting Software in Australia 2022 (Free & Paid) - SoftwareWorld

- Voluntary payments

- You can make a voluntary or early payment to offset a future liability. You can do this by BPAY® or direct credit using your EFT code. Alternatively, you can request a book of personalised payment slips from the ATO and use these to either pay over the counter at Australia Post or to send a cheque through the mail to the ATO.

MYOB Statement of Cash Flow report

MYOB has a report that sheds light on cash in and out for planning purposes.

- Access the report by going to the Reporting menu > Reports > Statement of cash flow report in the banking section. This will show:

- how your cash position has changed over a period of time

- the amount of cash earned from profit

- where you received additional cash, and

- where your cash was spent.

Notes:

- Once your accounts are classified (as Operating, Investing or Financing), they are displayed in that section of the report.

- In accounting terms, the Statement of Cash Flow report uses the 'indirect' or 'add-back' method to calculate the cash flows.

Check out the screenshot below with an explanatory table below it. This MYOB Business file does not have accounts set up as Investing or Financing, but if they had, they would appear on this report as well.

- A: You can toggle the Operating accounts to show or hide them

- B: This figure is the Net Profit/(Loss) amount from the Profit and Loss (Accrual) report.

- C: This section details changes in Asset and Liability accounts that are classified as Operating.

- D: This section details changes in Asset accounts that are classified as Bank.

Each of the government bodies mentioned here have extensive help sections. It's a good idea to set up a folder of bookmarks using the links provided below.

Accessing help when you need it

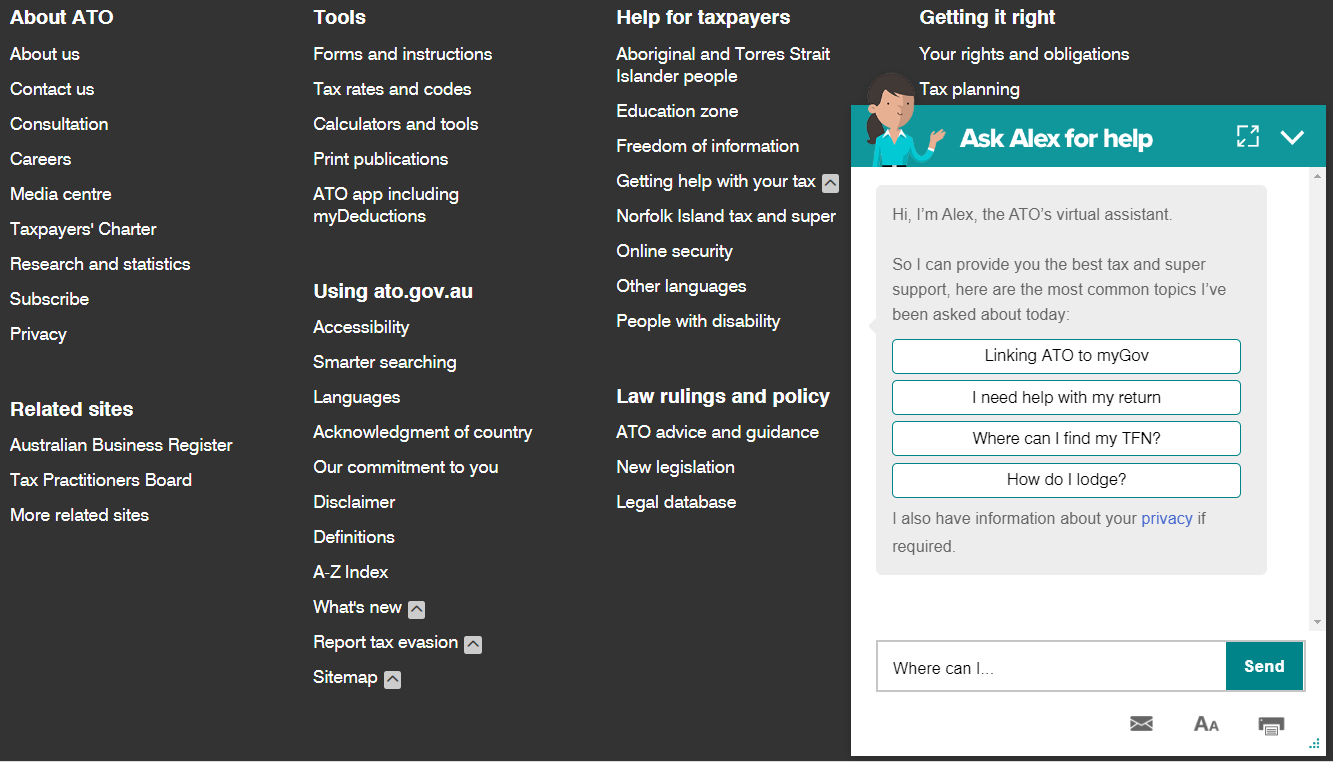

The Australian Taxation Office (ATO)

- Main website: ATO

- Their primary navigation will guide you to exactly where you need to go:

- The ATO has posted a list of other support sources on its links page.

- They also have an extensive footer with direct links to their most visited and helpful pages, as shown in the image below.

- And don't forget Alex, the ATO’s virtual assistant. You can always reach out by initiating a chat with Alex or selecting from the list of frequent support requests in the chatbox.

Tax Practitioners Board (TPB)

- Its main website

- Its main navigation provides two avenues with relevant information: Tax agents and BAS agents

Australian Charities and Not-for-profits Commission (ACNC)

- Its main website

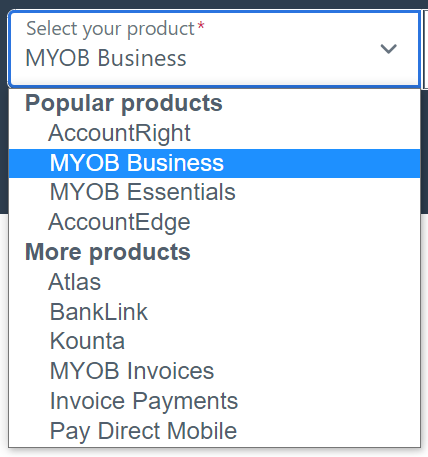

MYOB Business Help Centre

- The help pages at MYOB are robust and include some legislation requirements, accounting support and excellent technical support.

- The blog at MYOB for Accountants and bookkeepers provides excellent connection and support from your colleagues in the industry and is monitored by the support staff at MYOB.

- MYOB has an extensive help centre

- Ensure you have the correct software selected, MYOB Business

- Ensure you have the correct software selected, MYOB Business

YouTube

- MYOB has their own channel on YouTube

- Tax professionals and instructors have posted many videos. Once you find someone you like, you can subscribe to their channel.

Activity 1

Take some time and review a successful accounting agency's website, e-BAS accounts®

- Based on their homepage, who is their target audience?

- What services do they provide?

- Study the tasks and activities within those services. Were there concepts, terms, or abbreviations you didn't know?

- Read their blog entry titles, and choose two to read in entirety, then paraphrase the blog post in a one or two-paragraph essay.

Discuss your answers in the forum.

Activity 2

Scenario:

Imagine that you work for a company that buys electronic parts, builds them into a device and then sells them to the end consumer. You were hired because of your knowledge of technical products and sales, but the management team recognised your skills with finances and has been using you to do the books for a few years alongside your normal duties.

The business is now rapidly growing and bringing in a good revenue stream. Lately, when it comes time to pay their Activity Installments, there isn't any cash with which to pay, and the company falls short of its liability to the ATO. The role you were helping fill has become too cumbersome, and you believe they need to hire a qualified bookkeeper and BAS agent. The business already has a tax agent they use at tax time.

Write a proposal to the CEO that describes what you have been doing and why it makes sense to now outsource the role. Then suggest 3-5 businesses you compare and contrast and ultimately champion for your business to engage with.

Share your proposal on the Forum. Review and comment on others.