Codes of conduct are standards set of good industry practice for how people should behave or operate in a particular industry. The TPB enforces a strict code of conduct for BAS and tax agents.

Requirements to be a fit and proper person — to adhere to the code of conduct — start when a tax professional seeks registration. A person can be educated and experienced but also be untrustworthy and incompetent. One of the ways that the TPB protects consumers is to require that an agent must not have financially exploited the system or other clients or broken the law in the past five years.

As a reminder, a tax professional registrant must be able to show the TPB:

- The individual is of good fame, integrity, and character and has not been convicted of the following offences within the past five years:

- been convicted of a serious taxation offence

- been convicted of an offence involving fraud or dishonesty

- been penalised for being a promoter of a tax exploitation scheme

- been penalised for implementing a scheme that has been promoted based on conformity with a product ruling in a way that is materially different from that described in the product ruling

- had the status of an undischarged bankrupt

- been sentenced to a term of imprisonment, or served a term of imprisonment in whole or in part. 28

The full code:

- Review the Code of Conduct for BAS agents on the TPB Website

- Review the Code of Conduct for Tax agents on the TPB Website.

- Review the Code of Conduct for Accountants at the Chartered Accountants ANZ

Activities: Do you know the code?

Activity 1: Study the TPB code

Once you have studied the Code of Conduct for BAS agents on the TPB website, test your knowledge to confirm your understanding of the various code items.

Activity 2: Download a code policy

Download and study the ICB's code of professional conduct, then answer the questions below.

The five principles for BAS agents

The TPB's Code of Professional Conduct (Code) regulates BAS agents' personal and professional conduct.

The Code has five underlying principles:

You must act honestly and with integrity. You must comply with the taxation laws in the conduct of your personal affairs. You must account to your client for the money or other property if you:

- receive money or other property from or on behalf of a client, and

- hold the money or other property on trust.

You must act lawfully in the best interests of your client.

You must have in place adequate arrangements for the management of conflicts of interest that may arise in relation to the activities that you undertake in the capacity of a registered BAS agent.

You must act lawfully in the best interests of your client.

Unless you have a legal duty to do so, you must not disclose any information relating to a client’s affairs to a third party without your client’s permission.

You must act lawfully in the best interests of your client.

You must ensure that BAS services that you provide, or that is provided on your behalf, is provided competently.

You must maintain knowledge and skills relevant to the BAS services that you provide.

You must take reasonable care in ascertaining a client’s state of affairs, to the extent that ascertaining the state of those affairs is relevant to a statement you are making or a thing you are doing on behalf of a client.

You must take reasonable care to ensure that taxation laws are applied correctly to the circumstances in relation to which you are providing advice to a client.

You must act lawfully in the best interests of your client.

You must not knowingly obstruct the proper administration of the taxation laws.

You must advise your client of the client’s rights and obligations under the taxation laws that are materially related to the BAS services you provide.

You must maintain the professional indemnity insurance that the Board requires you to maintain.

You must respond to requests and directions from the Board in a timely, responsible and reasonable manner.

To read more about the Code of Professional Conduct access the TPB's Explanatory Paper on interpreting the Code contained in Division 30 of the TASA.

Professional Indemnity Insurance

There are several professions that require indemnity insurance. Those are generally services involving the use of a special skill or ability; for example, a designer may be accused of not working in the best interests of the client if they overstate their skills or experience - essentially charging for a service they are not performing well. Similarly, if you provide your clients with advice on finances or taxation, you are required by law to meet a particular level or standard expected of your profession. You can be held liable if loss or damage occurs as a consequence of you not meeting that standard.

As a BAS agent, professional indemnity insurance protects from claims made relating to the provision of professional advice or services.

Ethics in Accounting

When providing professional advice, employees in the financial services industry have a duty to provide advice and assistance which is competent and ethically sound. The client's interests are important, but there is a duty to act in the public interest, and not exclusively in the client's or employer's interests.

Ethical conduct is doing what is right, good, or fair in a specific situation. To demonstrate ethical behaviour, you must first weigh all relevant data, findings, and moral considerations (ethical values, standards, and obligations) before reaching a conclusion about what to do in specific situations or as a rule in your practice.

According to CPA Australia, these are the ethical considerations:

Ethical considerations29

- Avoid conflicts of interest.

- Maintain your client's confidentiality.

- Avoid contributing to the perpetration of unlawful acts.

- Ensure your client is well informed; give them comprehensive advice.

- Ensure your client understands the advice and has the capacity to act.

- Be respectful. With older clients, beware of ageism and the assumption that, because the client is old and perhaps frail, they are incapable of making a valid decision.

- Your client's best interests come first.

Managing a conflict of interest example

Scenario

Gina operates a math tutoring business and wants to hire a bookkeeper to assist her. She contacts her tax agent, Bradley, and asks him if he knows anyone. Bradley's wife is looking for side-work as a bookkeeper and she's good at what she does. Bradley suggests that "Rebecca" would be ideal, but fails to mention he's married to her because he fears that Gina won't trust the recommendation upon learning they are a couple.

The conflict of interest

Bradley has a personal and financial incentive in suggesting Rebecca as a bookkeeper.

Managing the conflict of interest

Instead, Bradley says and does this: "I have provided you with a list of recommended bookkeepers. I've put my wife, Rebecca, at the top of the list because she's excellent. She was a bookkeeper for ten years before we had children and is looking to get new clients so she can re-enter the workforce. That said, please feel free to explore any of the options on my list and choose the one that suits your working style."

Ensuring your client is well informed and has the capacity to act example

Scenario

Sean created a web development agency that has taken off. His gross income is $1.8 million. He's been looking to sell the business for months and finally found a prospective buyer. The buyer would like to offer jobs to the current employees, so he asks to see the personal, professional, and payroll history of Sean's staff before deciding to make the purchase or not. Sean reaches out to his tax agent, Bradley, and asks him to send the information along. Sean is concerned the employees will leave if they know he's trying to sell the company, so he asks Bradley to keep the secret and not disclose anything about it to his staff.

Obtaining Staff Permission

Sean's business is not legally required to comply with the Australian Privacy Principles because it is under the $3 million threshold. However, Bradley explains to Sean that all businesses should aim to comply with the privacy principles as a matter of best practice. He suggests Sean has two options, he can:

- come clean and discuss the situation with his staff

or - comply with the prospective buyer's request but without providing personally revealing details. That way, the new buyer knows the technical expertise of the staff, but not their names or contact details.

Bradley also suggests Sean creates a procedure in his business's privacy policy that documents the kinds of personal information the business holds, how it collects and stores that information, and for what purposes the information can be used.

Ethical dilemmas

If you haven't already, watch Alan Nelson discuss ethical dilemmas in accounting.

Ensuring your client is well informed and can act example

Scenario:

Sofia had been looking for her accounting business's first big client when she got a break — a large coin-operated laundry business with 10 locations across Australia looking for a new accountant. She gets the job, and upon starting, she notices that the income amounts vary dramatically in a highly suspicious way. Sofia is unsure how to proceed. Should she turn a blind eye or risk getting fired by initiating a difficult conversation with her new client so she can understand the cash flow idiosyncrasies more clearly?

What would you do?

Use the forum to explain what you would do as Sofia, including how you might approach the conversation with your client, and the reasons for your response, citing any professional legal and code of conduct responsibilities.

As a professional in the financial services industry, it is essential to keep abreast of legislation changes and remain competent in your industry as a tax professional. One of the ways to do that is to attend an accredited course.

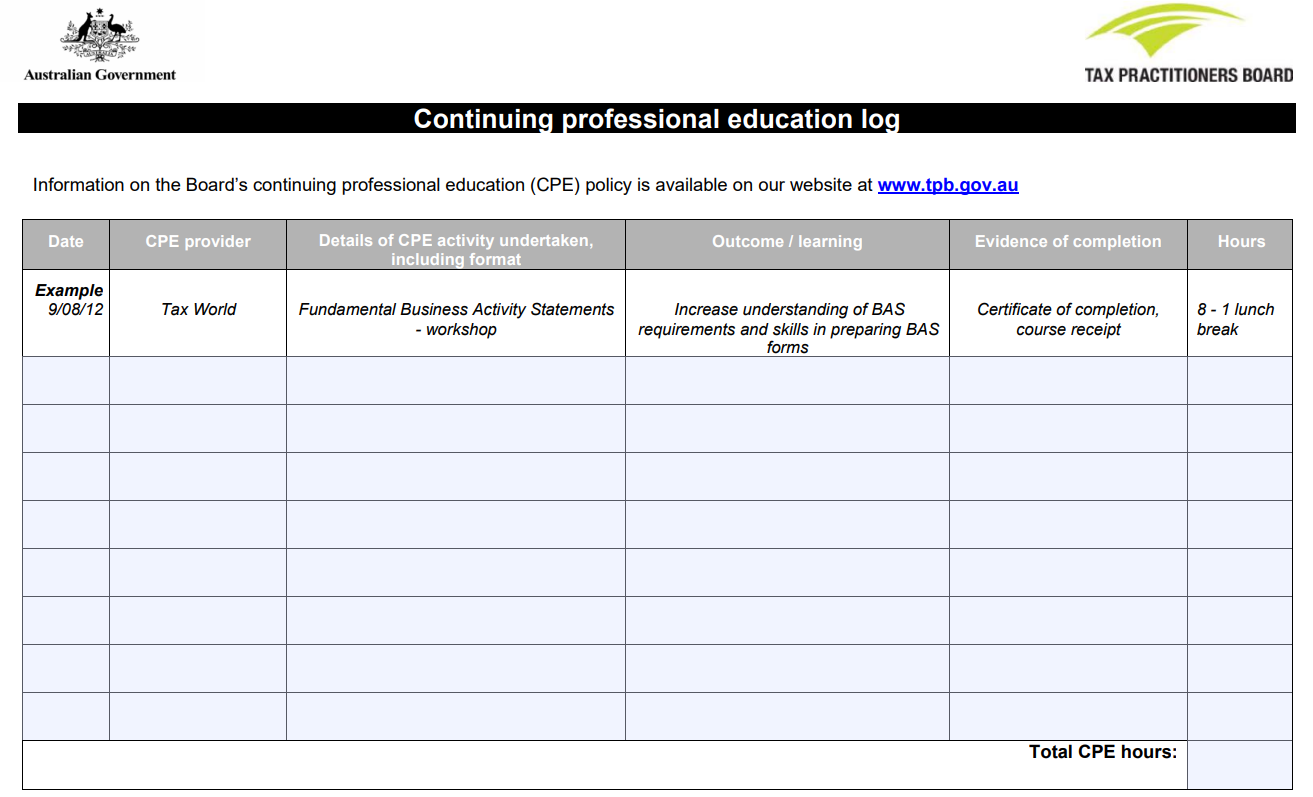

Continuing professional development for tax agents can mean ensuring that certifications and registrations are kept up to date.

BAS and tax agents are obligated by law to renew registrations and must complete continuing professional education (CPE) to maintain knowledge and skills. It is also an obligation under the Code of Professional Conduct.

The TPB provides these resources:

Track changes

You must keep track of your certificates, registrations, workshops, or related documentation as proof that these have been completed. Your LinkedIn profile serves the purpose of both professional visibility and a record of professional development.

Download this document to help you keep track of your professional development.

Research

To fulfil both legislative and professional requirements and remain updated, the Tax Agent Services Act (TASA) recommends many research methods that should be used to stay current. These are:

- Attending conferences and seminars

- Participating in online webinars

- Gaining membership in professional bodies

- Online research on specific aspects of BAS preparation and lodgment via ATO and other government sites

- Checking copies of legislation. E.g. the Goods and Services Tax (GST)

Websites and professional bodies that may be of interest include the following:

- The Tax Practitioners Board

- Australian Taxation Office

- Institute of Certified Bookkeepers

- Institute of Public Accountants

- Australian Bookkeepers’ Network

- Association of Accounting Technicians Australia

- Commonwealth legislation

- Chartered Accountants Australia | New Zealand - Learning tools

- The Tax Institute - staying up to date in tax laws

Stay on top of changes to Tax codes by bookmarking the information directly at the ATO on their pages:

If there are changes to the tax code, MYOB will update their tax codes page, so this is a great quick-access resource, whether you are using their accounting system or not.

Reading

- Brief subject overviews (such as those provided by the ATO)

- Recent scholarly articles, books

- Most Australian general tax textbooks will provide an introduction to all tax topics and refer to legislation, significant cases, and ATO tax rulings. As tax law constantly changes, make sure you use recently published books. These can be found in the High Use Collection in the Law Library.

- Blogs

- MYOB's Blog

- Feedspot's blog of blogs

Policy is incredibly important, it sets out the guiding principles and the foundational ideas for legislation, for budget allocations, and it is the foundation from which actions flow, by government, by businesses often and NGOs.Professor Robynne Quiggin, Professor of Indigenous Policy at the UTS Institute for Public Policy and Governance30

Apply policies about compliance with the code of professional conduct

An accounting or tax professional organisation should have policies related to compliance with tax activities.

For example, a finance policy outlines the procedures to be followed for undertaking financial dealings with the business. The policy provides the rules and fundamental truth of the business's vision and values. The procedures described in the policy provide directions that specify what each employee must do to comply with the policy.

We recommend financial organisations develop policies that ensure compliance with codes of professional conduct. Here are some examples of that:

- Reporting and timing

- Recordkeeping

- Professional development

- Hiring

The TPB offers specific guidance for policy consideration and creation:

- Engaging clients: Bringing on new clients is a time for a business to elicit confidence in the agent's skills and qualifications. Ensuring the procedures involved comply with legislation and match the vision of the business's public face.

- Acting lawfully in the clients' best interests: As a fundamental requirement, the TPB provides guidance to comply with and deliver best practices and standards for clients.

- Managing conflicts of interest: Having policies around ethical considerations means the leadership of the business communicates to their staff the standards for managing any situation.

- Client information privacy: Short version: you need the client's permission before giving away their information.

Creating policy

Here are a few example policies for you to review:

- Template Financial Policy from Business Victoria

- ATO Privacy Policy - The ATO's privacy policy.

How to write your financial policy manual31

- Start by thinking about what you want to achieve.

- Get your employees involved.

- Write down your policies and procedures as you do each activity throughout the day.

- For example, if you have a new customer, write up how you'll record the details, where these will be kept, how you'll set a customer credit limit and any other standards you want to set.

Activities: Put yourself in the shoes of an acting BAS agent

Scenario

Think back to the previous activity where you were championing for a different accountancy firm to take over the books of your tech company and relieve you of those duties.

One of the issues brought up when looking for an outsourced option is that there are insufficient funds available to pay tax liabilities when they become due. Describe what you have to do if you miss a payment deadline - what are the consequences? Write an email to management explaining the problem and how it can be rectified if the business does not outsource accounting.

Share the email with the forum and comment on others.

Activity 2

Pick an accountancy firm and explore its website. Based on what you can pick up, identify at least two ways they are complying with the TPB code of conduct, and how they acknowledge their duties to the Privacy Act. Use language from the Privacy Act to explain your position.

Share your answers on the forum and comment on others.

Activity 3

Do you know where to turn to for help?